Keeping with our theme of stocks in the 'No-Buy Zone'...

Just because a company went public as a special purpose acquisition company ("SPAC") during the peak of the frenzy doesn't necessarily mean it's an accident waiting to happen...

That's because the vast majority of these SPACs have already crashed.

Of the entire 197 members of SPAC Class of 2021 that still exist, only 14 are still trading above the price when they merged with a "real" company.

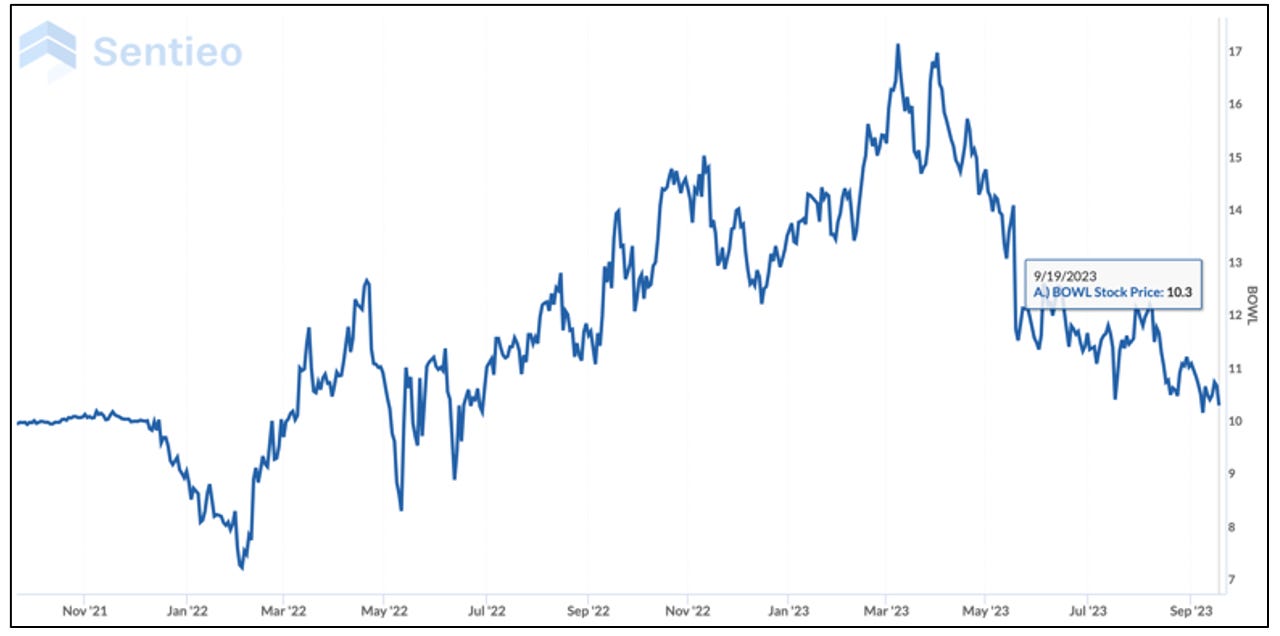

Of those, keep an eye on Bowlero (BOWL), a rollup of bowling alleys...

With its stock still hovering just barely above $10 per share, Bowlero claims to be the world's largest operator of bowling centers, with 345 units in 36 states. Most are what it calls "upscale entertainment concepts with lounge seating, arcades, enhanced food and beverage offerings."

The company had seemed to be on a roll, with same-store sales reaching more than 30% at their peak...

But that was during the "reopening" as the world was rebounding from the pandemic... and like all things leisure and recreation, business was booming.

Business was so good that Bowlero started raising prices, with one price increase after the other... because it could. In some cases, when demand was so high, it even added what it called "peak” or surge pricing.

It was the kind of story investors love...

Rising prices, rising margins, rising same-store sales... all on a company with high fixed costs, which means anything above and beyond was cream.

It was quite a story, and management told it quite well – as founder and CEO Tom Shannon's did on the September 2022 earnings call, when he said (emphasis added)...

I think we can continue to grow margin for a really long time because as you say, in this inflationary environment, we're raising prices on everything, but we don't have cost of goods sold on the majority of our revenue.

But then, he added the big asterisk, when he said in the very next breath (emphasis added)...

So I think we're going to continue to see margin improvement. It may not be as great as it has been historically because we do have other input costs rising on the food, beverage, utilities, labor, etc. But I think we're very fortunate that our business model is designed in a way that really minimizes input costs and maximizes operating profit.

In other words, like all parties – especially those post-pandemic – this one was bound to end...

By the time Bowlero reported its fourth quarter a week ago, after quarters of rising at double-, even triple-digit rates, sales growth had tumbled by 10.5%. And while the company reported $146.2 million in earnings for the period, up from a meager $6 million the year before, more than half was from a tax benefit.

As with any retailer or restaurant – or a company like Bowlero – the real story is same-store sales, which the company said fell by 2.6%...

Equally worrisome were margins, which supposedly could "grow for a very long time." They plummeted, with operating margins hitting 8% versus 17% a year earlier... back when the company was touting its pricing power and the potential for its margins.

It gets worse...

For Bowlero, the more games a customer bowls and the longer they stay, the more likely they are to buy more food or play games at the arcade, which its bowling centers have.

During the pandemic, people had nothing else to do, so they stayed longer... and "most of our center associates were order takers and service providers, with no requirement to sell."

Now, as business has slowed, bowling center employees are becoming salespeople... hawking "a bundled offering called 'The Special,'“ which Shannon says “allows guests to prepay for a third game at a discounted price and receive a complimentary $5 card to encourage ancillary spending."

Here's a company that once was so busy that it implemented surge pricing, and now it's offering discounts.

CFO Bobby Lavan calls the special “a silent price increase,” with a 60% take rate...

And maybe it is, but he went on to say something investors in any company hooked on price increases never want to see management say...

Ultimately, the days of mid- to high single-digit price increases are behind us.

At the same time, it seems that customers are now hooked on discounts... so much so that Bowlero said it realized that in recent months it had "pulled back too hard on midweek and late-night promotions," implying traffic fell off when it did. It has since started to “reactivate” them.

That’s right… not only does it appear that Bowlero no longer has pricing power, but its customers are demanding cheaper prices. Not a good look…

Meanwhile, net debt is increasing, and as (you might guess) so are interest expenses. Much of the current debt, which expires in 2028, is at a variable rate that currently hovers at close 8.65%.

The company says it is looking at lower cost funding sources, including possibly selling some of its "unencumbered real estate."

At the same time, based on the need "to raise the bar of talent and retain our associates," labor costs have shot higher.

No wonder insiders including Shannon were selling earlier this year at or near highs.

There are other issues, as well, but a few go in the category of “interesting”...

One has to do with some numbers that have been changed in regulatory filings with no explanation.

The table below shows a difference in the numbers reported by the company in its reporting of fiscal 2022 same-store center revenues and revenues for media.

I’m sure there’s a good explanation, but interesting, nonetheless.

Equally intriguing…

Earlier this year there was a transaction between CEO Shannon and board member Sandeep Mathrani, who recently left his post as CEO of WeWork (WE) – the troubled shared office space company.

At Bowlero, Mathrani isn't just any board member... but also a member of the audit and compensation committees. One oversees financial reporting and related internal controls, risk, ethics, and compliance… the other, executive compensation.

Shannon and Mathrani, it turns out, are neighbors in Miami Beach. Earlier this year, according to press reports, Mathrani sold his condo to Shannon, for $21 million.

It's quite an upgrade for Shannon, who bought a unit in the same building in 2019 for a paltry $6.4 million.

Based on the size of his stock sales, Shannon can clearly cover the difference.

Even without them, he’s well compensated. In fiscal 2022, Shannon’s total compensation was $67 million. That includes options and stock awards, but also a $14 million bonus tied to the SPAC merger and his regular salary of $1.2 million.

Here's the thing...

The money is going to a member of his audit and compensation committee… somebody who is involved in deciding how much money he’ll make while also playing a role in oversight of the company’s internal controls. Like those inconsistent numbers above… it’s worth noting.

► My bottom line...

Bowling as the next big thing is a great story. Except… this isn’t the first time it has caught Wall Street’s fascination. It just never has seemed too be able to go the distance, at least not sustainably so...

As recently as 2018, in its series on struggling sports, USA Today ran a story headlined, "Rolling Along: Bowling industry tries to reverse its downhill trend."

Over my career, I've covered some of these bowling companies and their supposed revivals, like Brunswick's (BC) bowling centers. (Now owned by Bowlero, after being spun off by its parent, which chose boating over bowling.) Or AMF, which went on to file for bankruptcy after going public in the stock market bubble of 1997. (It, too, is now owned by Bowlero.)

Bowlero went public in the 2021 stock market bubble… in a near-zero interest world, when debt for acquisitions was free and people were looking for something fun to do.

Now, debt costs real money... and like many of us who have bowled here and there during our lives, people got bored and moved on to other things.

There will always be core bowlers and bowling leagues. And teens looking for a place to have clean fun. And what family with little kids hasn't played Bumper Bowling?

Now Bowlero has to prove that as life goes on for the rest of us, bowling as a growth industry will, too.

Falling rates will help, especially on the debt and interest rate side, but a recession (if there is one) won't. That, in fact, is what did in AMF.

Management, for its part, points out that Bowlero generates more than enough cash to reinvest in itself and says that the company has “a long runway of opportunities...”

It very well may, but with thousands of public companies to choose from – and given the uncertainties it faces and how swiftly its business model has been stressed... Avoid.

As always, if you have an opposing view, feel free to let me know. Just keep it above the belt.

Disclosure: I have no position in this stock.

If you liked reading today’s Herb on the Street, let me know by hitting that heart button below… and feel free to share this with your friends and if you haven’t done so already, subscribe.

I welcome feedback, comments or an ideas. Feel free to contact me at herbgreenberg@substack.com. You can follow me on Twitter and Threads @herbgreenberg.

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice.

Really nice take. I wonder if this could be a microcosm of the wider consumer economy over the last year or two. People seemed to be willing to pay any price coming out of the pandemic be it airline fares, potato chips, steak sandwiches, houses, cars, or coke. Maybe this is some kind of post-pandemic psychology where the US consumer, who is not known for great price discipline has had zero.

In a world where credit card servicing costs are up substantially with wages slowing that might be ready to change. To this point I have felt like I’m the only one saying no to a 6 dollar bag of Doritos. Do people really want to pay 25% credit card interest rates for that?