Red Flag Alert Update – Crossing the Foul Line

Bowlero strikes again

***Head’s up: Big changes are coming to On the Street. We’re evolving, expanding... reimagining. Stay tuned!***

Dividends are back in vogue, but be careful...

Some companies simply shouldn’t being paying them.

And when they do, especially if they’re loaded with debt, they have negative free cash flow and their financial metrics are going the wrong, it’s an obvious red flag.

When that company owns bowling alleys, and has growing cash needs as it tries to expand through acquisition and new builds, it’s akin to crossing the foul line.

Enter Bowlero ($BOWL), no stranger to readers of my Red Flag Alerts.

I first red-flagged the company in September based on slowing growth, falling margins, rising debt and a business model tied to rolling up an industry that historically has proven to be a lousy investment.

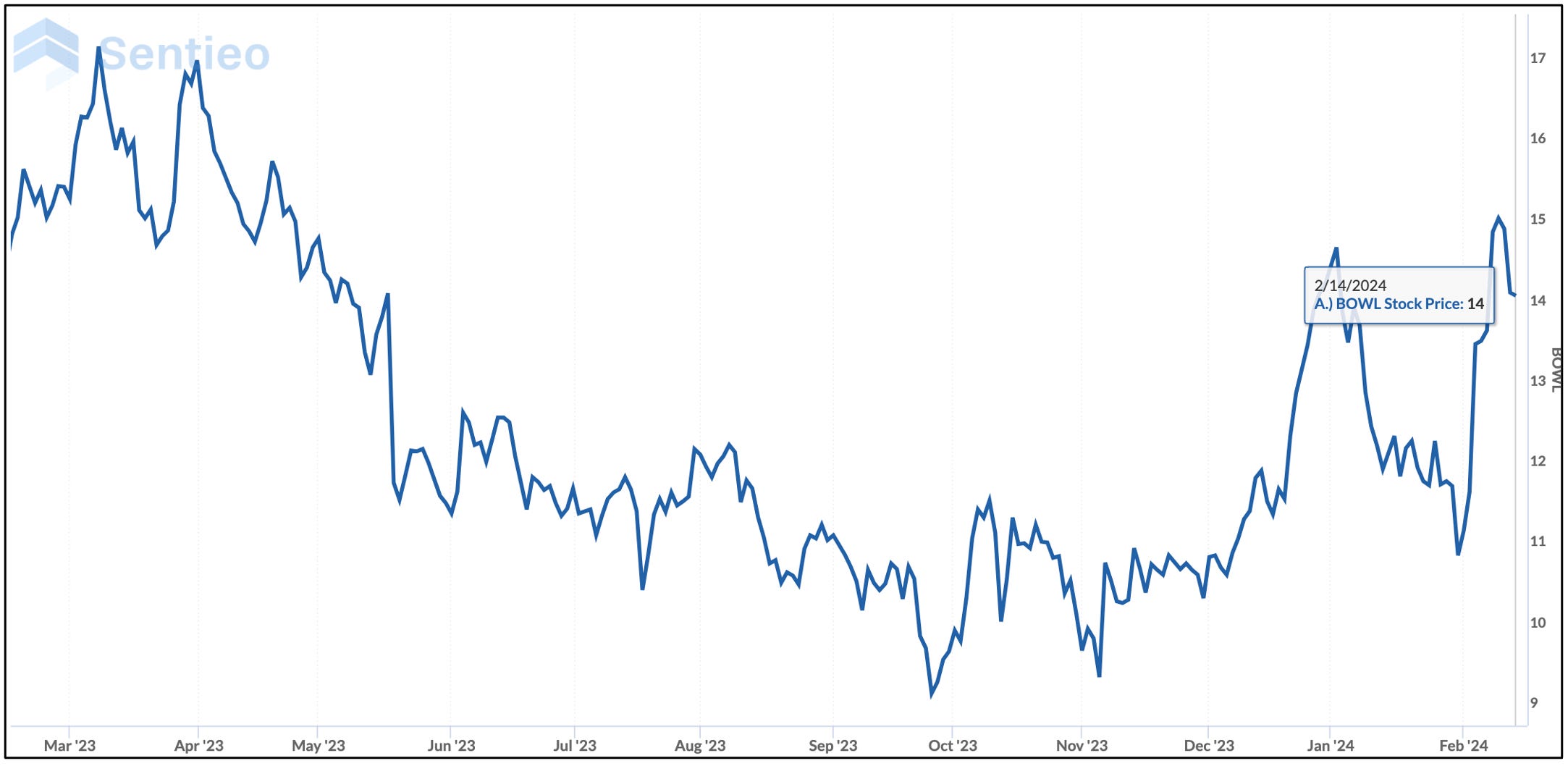

But here we are, five months later. And after its stock had been bobbing around, before recently pulling back it had skyrocketed nearly 40%... in less than two weeks.

It’s not because its business has miraculously reversed itself. It’s because (drumroll!)... it has so much cash not to spend – (sarcasm) – that in addition to actively buying back its shares, it initiated a dividend on its common stock.

Bowlero 101

Before we go further, this quick refresher: Bowlero went public in 2021 as a SPAC. It’s a rollup of bowling alleys. The timing couldn’t have been better…

Like similar entertainment-type venues, as lockdowns were relaxed and people wanted to get out, bowling became hot. So hot that booking time at a bowling alley sparked surge-like pricing. Bowlero kept raising prices for no other reason than... it could. Things were going so well that at one point its same-store sales were growing at 30%.

Then came the post-Covid hangover….

Bowling did as it has a history of doing over the decades: As a fad, it faded.