Tupperware – Hold the Confetti

With its stock soaring by as much as 50% Friday, it’s clear Tupperware investors were having a party...

They obviously were cheering news that the company has reached a deal with its banks to restructure its debt.

But after going over the filing with a friend who used to be a credit analyst, I’d say these investors might want to hold the confetti.

Not that it matters with a stock like this, which trades on everything but fundamentals.

What else would explain the action of the past few weeks, especially on Friday... likely the result of a press release announcing the debt restructuring.

I’m pretty sure most anybody who bought the stock never got beyond the headline... certainly not to the actual debt agreement – and that’s assuming they saw either. (Doubtful.)

And if they did, they likely wouldn’t know the real significance.

I know I wouldn’t, especially the nuances, because I’m not a debt guy..

But my friend is a debt guy, and with his help here’s what really appears to be going on with Tupperware.

The restructuring of more than $500 million in debt involves a consortium of banks, led by Wells Fargo. It appears the banks had little choice but to either let the company file for bankruptcy reorganization (it was in violation of loan covenants) or give it one last chance to turn itself around.

The banks chose the latter. But taking a closer look at the deal, the structure is somewhat similar to what you might see in a bankruptcy, just without formally filing for bankruptcy.

So, for example, similar to a bankruptcy, the banks are receiving warrants, which once exercised gives them the right to hold or sell the stock. It’s a sweetener, so in the event of a total blowup, they might not walk away entirely empty-handed.

In this deal, the warrants are equal to 4.99% of the outstanding and issued Tupperware stock. That, in itself, is interesting, since anything above 4.99% would require the banks to disclose any changes in their holdings.

But there’s a twist...

As part of the deal, as of last Wednesday the banks had the right to “immediately” exercise 60% of those warrants. If they did that means in all likelihood they very well may have been sold on the stock’s run-up...

And if they did, that means as much as roughly an additional 1.4 million shares would be added to Tupperware’s share count, in turn diluting existing investors.

But don’t lose sight of this...

Even with this restructuring, Tupperware’s stock remains highly speculative…

Terms of the credit agreement include provisions for bankruptcy and default, and including wording in the event shares no longer actively trade on the New York Stock Exchange… or anywhere.

In the press release announcing the restructuring, here’s what CFO Mariela Matute said…

I am confident that this agreement provides us with the financial flexibility to continue executing on our near-term turnaround efforts as well as our long-term strategy to create a global omni-channel consumer brand.

That sounds encouraging, except this is a company that has been talking about turning itself around for more than 20 years.

I first ran into Tupperware in the mid-1980s when I was covering Dart & Kraft while I was a reporter for the Chicago Tribune.

Kraft had merged with Dart Industries, which owned Tupperware – then a star of the show. But pretty soon Tupperware started to sputter, the result (it was said at the time) of more women working outside of the home. This was the first sign the business model was breaking.

As the Wall Street Journal recalled in a 2017 obituary of former Kraft CEO John Richman…

Tupperware proved a disappointment. Profits began falling as more women joined the workforce and weren’t available for the home Tupperware “parties” at which the plastic food containers were sold. Dart & Kraft tried to smarten up the product, making it safe for microwaves, and promised Tupperware parties during office lunch breaks. But the brand kept floundering.

Since then, Tupperware been handed over from company to another until being spun off.

It has been trying to turn itself around ever since… And current management, which arrived in 2020, had a turnaround plan, too.

So far, as the numbers show, whatever they’re doing hasn’t worked...

As I’ve written over and over and over again, Tupperware’s direct-sales business model is now officially broken. Look no further than its revenues, as this 10-year chart clearly shows...

You might have noticed that the chart is missing the past two quarters. That’s because the company hasn’t formally reported earnings since the fourth quarter... and hasn’t filed any formal financials with the SEC since last November.

But new numbers suggest the situation has gone from not good to bad… and now, worse.

In two filings last Thursday, including one notifying regulators that its second quarter 10-Q would be late, Tupperware disclosed that revenue for the quarter would be around $265 million. That’s down from an estimated $285 million in the first quarter (included in the notification of that quarter’s delayed filing) and 22% below the year-ago quarter... and 44% below the same quarter in 2019, pre-pandemic.

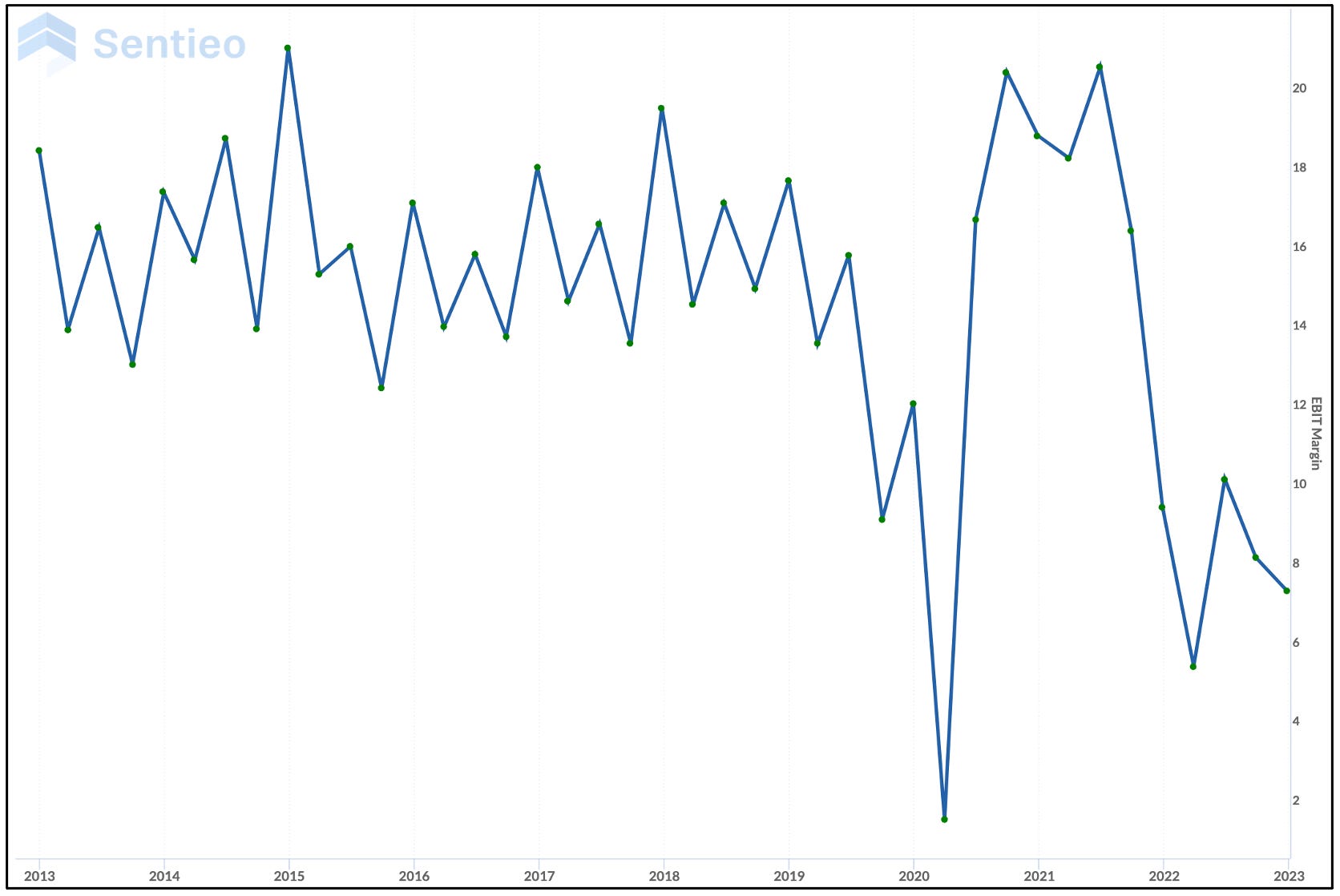

The story is much the same with adjusted operating margins, which have been crushed. (I’m using adjusted numbers, because they give the company the benefit of the doubt... in theory making things look their very best.)

As the chart shows, even before the pandemic, the profitability trend was not Tupperware’s friend. Covid gave the company a brief respite, as the stay-at-home trend appeared to give the business model a new lease on life.

But it was an illusion...

In an effort to revive things, Tupperware’s “turnaround plan” includes selling some of its products at retail, starting with Target.

The trouble is, that puts the company in direct head-to-head competition with rivals in a price-conscious, crowded space... while at the same time cannibalizing potential sales from the Tupperware Party crowd.

Here’s where it could get interesting...

Through all of this, Tupperware has said it will likely have to restate its financial statements going back to 2020... that’s right, back to when sales and profits suddenly exploded higher.

There is, no doubt, a great story buried in there somewhere... especially since the company has delayed the completion of the restatement to late September from mid-July. But the reality is, the restatement might not matter. For years, restatements (even fraud) often have been greeted by Wall Street with a giant yawn, as investors view them as old news.

On the bright side, the restatement arguably could be viewed as giving Tupperware management a clean slate, setting the stage for a reset of its already broken business model.

However, outside of the iconic and ubiquitous nature of its brand, Tupperware will face intense competition...

And it’s the very competition that has made direct sales of its products so difficult. That, in turn, will likely resulting in even lower margins. (For just how bad things could get, take a look at Newell Brands with Rubbermaid, which hasn’t been able to get out of its own way for at least seven years.)

Even at Target, it competes head-to-head with Target’s Up & Up house brand, which sells at a lower price point.

Then there’s the replacement issue: Food storage containers often last for years, which is why in its heyday (and even today) Tupperware kept creating line extensions – from ice cube trays to butter dishes… plastic products might create an impulsive sale at a party, but not so much online or elsewhere.

Still, it is Tupperware, and if all else fails there’s a ready buyer out there for the company or – if that doesn’t make it – just the brand.

Then again, at what price? Tupperware currently has a market value of just over $200 million. It also has more than $500 million in debt, with negligible or no profits and sales growth decelerating at a rapid pace.

Before we go, one other thing...

Over the past week, as the stock has been rising on no news, I suggested that if there was something going on at the company that hadn’t yet been disclosed, there very well may be illegal insider trading.

Given the timing of the announcement of this debt restructuring, the only question I have is: Who knew what, when? It would appear that somebody clearly knew something.

I’ll take it one step further…

If you didn’t know better, you might even think these kind of debt restructurings of companies with big, well-known brands are part of a deliberate (and I’d say brilliant) strategy…

It’s a strategy designed to stoke the emotions of the Robinhood investing crowd, which in turn helps goose these types of stocks higher, with the express intention of bailing somebody out.

There I go with my silly conspiracies again. Onward.

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts, and should not be construed as investment advice.

I can be reached at herb@herbgreenberg.com.

I was thinking maybe Martha Stewart.

So would someone buy their name. Byrne at Overstock bought BBB for the name?